History suggests the best protection comes from diversified investing, including a meaningful allocation to steady stocks

IMAGINE receiving $1 million today, along with the responsibility to safeguard and grow it over the next decade. Your primary goal: preserve its real value – and ideally increase it. How would you allocate this capital?

There is no straightforward answer. History shows that even the most secure-seeming options carry hidden risks.

Capital at risk, always

US financial data from 1900 to 2024 shows that inflation averaged 3 per cent a year. This means over a century, one dollar eroded to less than four cents – a loss of more than 96 per cent in purchasing power.

What if you put your cash in a savings account? That gives you interest and feels safer. Over the past century, savings accounts in countries like the US and other western nations have on average kept pace with inflation. Short-term saving rates, proxied by short-term US T-bills, averaged 3 per cent a year.

Averages mask significant losses, however. Financial repression in the 1940s and early 1950s saw interest rates being held artificially low while prices crept higher. This was done to lower the debt of governments heavily indebted after World War II. Savers suffered a real loss in purchasing power of more than 40 per cent.

As at 2025, a new era of financial repression appears to be underway. The inflation spike of 2022, combined with interest rates lagging behind, caused a real loss in value of nearly 20 per cent. Savers are still down about 10 per cent relative to 2010 levels. With real interest rates near zero in 2025, catching up will be difficult.

These episodes underscore a fundamental truth: even assets that feel safe – like savings accounts – can expose investors to real, lasting losses. That brings us to a broader point – capital is always at risk. Whether you choose to save or invest, you’re making a bet. Inflation and market volatility are ever-present.

Government bonds: Safer, but safe enough?

For many investors, the next step beyond saving is government bonds. They typically offer about 1 per cent more yield than a savings account and are often viewed as a safer alternative to equities. But safe from what?

Bond investors have faced challenging periods since 1900. After World War I, a post-war economic boom led to rising inflation, which eroded the purchasing power of government bonds issued during the war.

A similar pattern followed World War II – artificially low interest rates and a prolonged bond bear market. Then came the “bond winter” of the 1970s, when bondholders lost nearly 50 per cent in real terms. That’s not just volatility, that’s wealth destruction. Remember: it takes a 100 per cent gain to recover from a 50 per cent loss.

As of 2025, investors are once again in a “bond winter”, facing a cumulative real loss of around 30 per cent, driven by the high inflation of the early 2020s and the subsequent rise in bond yields.

Stocks: Long-term gain, long-term pain

Stocks can really disappoint in both the short term and the long run. Not every dip is followed by a swift recovery. Inflation can further erode real returns.

The 21st century alone had three drawdowns of more than 30 per cent in real terms. These huge and frequent losses are a feature of stock markets and thus, most investors are well aware of the short-term risks.

Over the long term, equities deliver higher returns than bonds. Yet, over multi-decade horizons, equities can still disappoint. Recent research by Edward McQuarrie suggests that even in the 19th century, stocks did not consistently outperform bonds, challenging the assumption that equities are always the safest long-term investment.

Comparing asset classes

We examine real losses – the decline in purchasing power – across four key asset classes: savings accounts, government bonds, gold and equities. We look at both short-term (one-year) and long-term (10-year) risk using the conditional value at risk (CVar), a measure of average losses in the worst periods. This measures the expected loss in the worst periods.

Savings accounts can quietly erode wealth over time. The accompanying graphic highlights a key paradox – savings are comparatively safe in the short run, but are far from secure over longer horizons.

Bonds offered somewhat better long-term performance, but with deeper short-term drawdowns.

Gold, often viewed as a safe haven, is volatile in both the short and long run. Despite this, it can still serve as a useful diversifier, particularly when combined with steady or low-volatility stocks.

Equities deliver the highest long-term returns, but also the greatest drawdowns. Long-term investors are rewarded – but only if they can endure severe interim declines.

These long-term numbers are rarely shown – and for good reason. Most empirical research focuses on short-term, nominal returns, which offer more statistical power but assume investors only care about monthly volatility. When viewed through real, long-term lens, a very different picture emerges.

The takeaway is simple. In the long run, all investments are risky. What matters most is not whether you face risk, but how you manage this risk.

A middle way via steady stocks

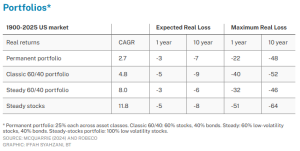

Once you have capital, you’re exposed to risk – whether you save or invest. The good news is that risk can be reduced through diversification across asset classes: bonds, equities, savings and even gold. This is one of the few “free lunches” in finance, reducing risk without sacrificing return. Yet, even in a classic 60/40 (60 per cent bonds, 40 per cent stocks) portfolio, most of the risk still comes from equities.

There is a better way: reduce stock market risk by focusing on stable companies, sometimes called “widow-and-orphan” or steady stocks. These firms tend to deliver consistent returns, much like bonds, but with an important advantage – their earnings can grow with inflation. These low-volatility stocks may lag during strong bull markets, but they tend to hold up better during downturns.

The second graphic makes a strong case for both diversification and steady stocks. A portfolio fully allocated to steady stocks exhibits similar expected losses as a traditional or classic 60/40 portfolio. Yet, being fully invested in stocks means tail risk which is apparent since the maximum real losses are higher for steady stocks than for the classic 60/40 mix.

Therefore, a steady 60/40 portfolio deserves attention. This portfolio invests in defensive equities and has lower downside risk, comparable to the ultra-conservative permanent portfolio (which invests 25 per cent equally in stocks, bonds, savings and gold), but with meaningfully higher returns.

The safest move: Lose less

Even the safest investment will lose value at some point. But some portfolios lose less, and losing less gives investors the time and confidence to stay invested.

Now imagine again being entrusted with $1 million to preserve and grow over the next decade. You now recognise that it’s not an easy task but a balancing act. History suggests the best protection comes from diversified investing, including a meaningful allocation to steady stocks.

The writer (PhD) is head of conservative equities and chief quant strategist, Robeco. This content has been adapted from an article that first appeared on CFA Institute Enterprising Investor at https://blogs.cfainstitute.org/investor/